Entering transactions in the general journal and posting them to the correct general ledger accounts is time consuming. In the general journal, a simple transaction requires three lines—two to list the accounts and one to describe the transaction. The transaction must then be posted to each general ledger account. If the transaction affects a control account, the posting must be done twice—once to the subsidiary ledger account and once to the controlling general ledger account. To speed up this process, companies use special journals to record repetitive transactions that affect the same set of accounts and have a consistent description. Such transactions can be documented on one line in a special journal. Then, instead of separately posting individual entries, each column's total is posted at the end of the accounting period.

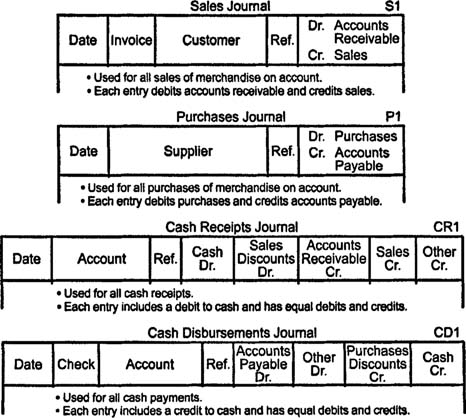

Although companies create special journals for other types of repetitive transactions, almost all merchandising companies use special journals for sales, purchases, cash receipts, and cash disbursements.

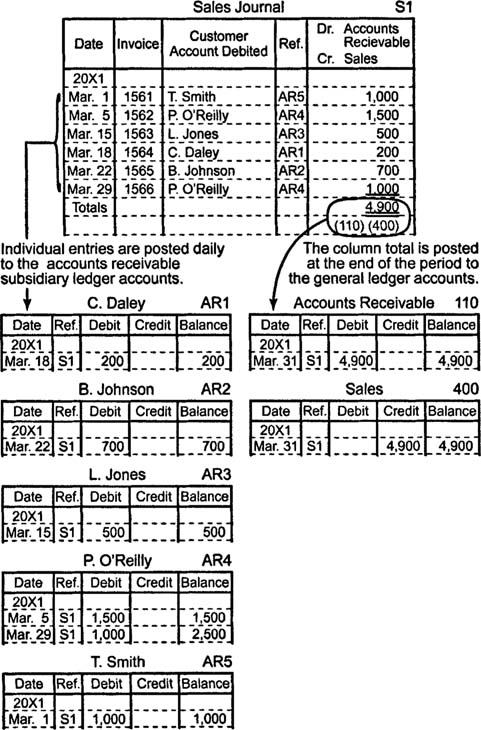

Sales journal. The sales journal lists all credit sales made to customers. Sales returns and cash sales are not recorded in this journal. Entries in the sales journal typically include the date, invoice number, customer name, and amount. Invoices are the source documents that provide this information. In its most basic form, a sales journal has only one column for recording transaction amounts. Each entry increases (debits) accounts receivable and increases (credits) sales.

Notice the dates and posting references applied to each entry in the illustration to the right. Each day, individual sales journal entries are posted to the accounts receivable subsidiary ledger accounts so that customer balances remain current. Customer account numbers (or check marks if customer accounts are simply kept in alphabetical order) are placed in the sales journal's reference column to indicate that the entries have been posted. At the end of the accounting period, the column total is posted to the accounts receivable and sales accounts in the general ledger. Account numbers are placed in parentheses below the column to indicate that the total has been posted.

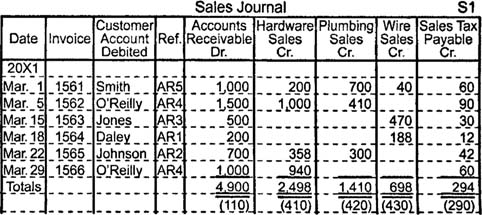

Many companies use a multi‐column (columnar) sales journal that provides separate columns for specific sales accounts and for sales tax payable. Each line in a multi‐column journal must contain equal debits and credits. For example, the entries in the sales journal to the right appear below in a multi‐column sales journal that tracks hardware sales, plumbing sales, wire sales, and sales tax payable. Individual entries are still posted daily to the accounts receivable subsidiary ledger accounts, and each column total is posted at the end of the accounting period to the appropriate general ledger account.

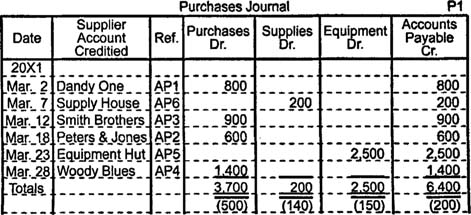

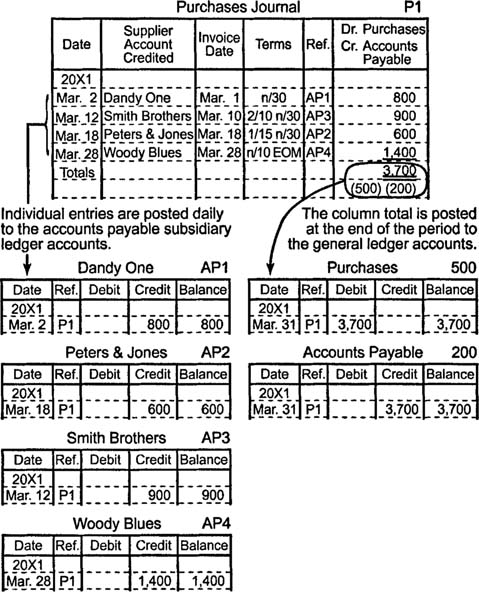

Purchases journal. The purchases journal lists all credit purchases of merchandise. Entries in this journal usually include the date of the entry, the name of the supplier, and the amount of the transaction. Some companies include columns to identify the invoice date and credit terms, thereby making the purchases journal a tool that helps the companies take advantage of discounts just before they expire. The purchases journal to the right has only one column for recording transaction amounts. Each entry increases (debits) purchases and increases (credits) accounts payable.

Each day, individual entries are posted to the accounts payable subsidiary ledger accounts. Creditor account numbers (or check marks if the creditor accounts are not numbered) are placed in the purchases journal's reference column to indicate that the entries have been posted. At the end of the accounting period, the column total is posted to purchases and accounts payable in the general ledger. Account numbers are placed in parentheses below the column to indicate that the total has been posted.

Companies that frequently make credit purchases of items other than merchandise use a multi‐column purchases journal. For example, the purchases journal below includes columns for supplies and equipment. Of course, every purchase in the journal below must credit accounts payable; equipment purchased with a note payable or supplies purchased with cash would not be recorded in this journal. Individual entries are still posted daily to the accounts payable subsidiary ledger accounts, and each column total is posted at the end of the accounting period to the appropriate general ledger account.

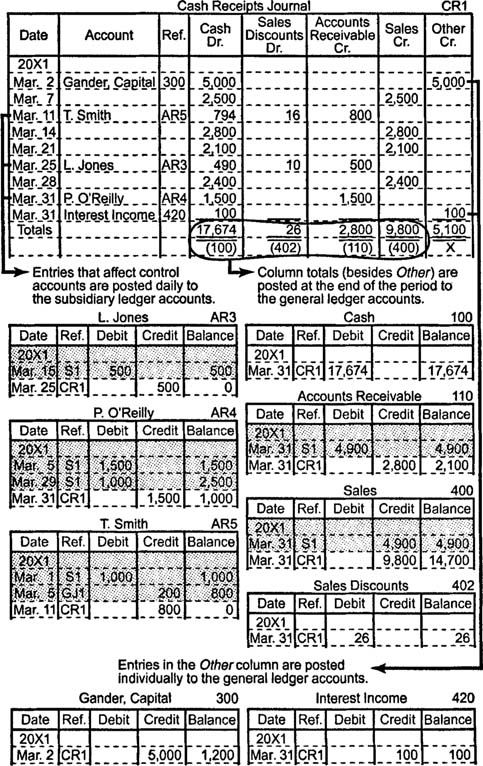

Cash receipts journal. Transactions that increase cash are recorded in a multi‐column cash receipts journal. If sales discounts are offered to customers, the journal includes a separate debit column for sales discounts. Credit columns for accounts receivable and for sales are normally present, but companies that frequently receive cash from other, specific sources use additional columns to record those types of cash receipts. In addition, the cash receipts journal includes a column named Other, which is used to record various types of cash receipts that occur infrequently and therefore do not warrant a separate column. For example, cash receipts from capital investments, bank loans, and interest revenues are generally recorded in the Other column. However, a company that provides consumer loans and receives interest payments from many customers would probably include a separate column for interest revenue. Whenever a credit entry affects accounts receivable or appears in the Other column, the specific account is identified in the column named Account.

Accounts receivable payments are posted daily to the individual subsidiary ledger accounts, and customer account numbers (or check marks if the customer accounts are not numbered) are placed in the cash receipts journal's reference column. At the end of the accounting period, each column total is posted to the general ledger account listed at the top of the column, and the account number is placed in parentheses below the total. Entries in the Other column are posted individually to the general ledger accounts affected, and the account numbers are placed in the cash receipts journal's reference column. A capital X is placed below the Other column to indicate that the column total cannot be posted to a general ledger account.

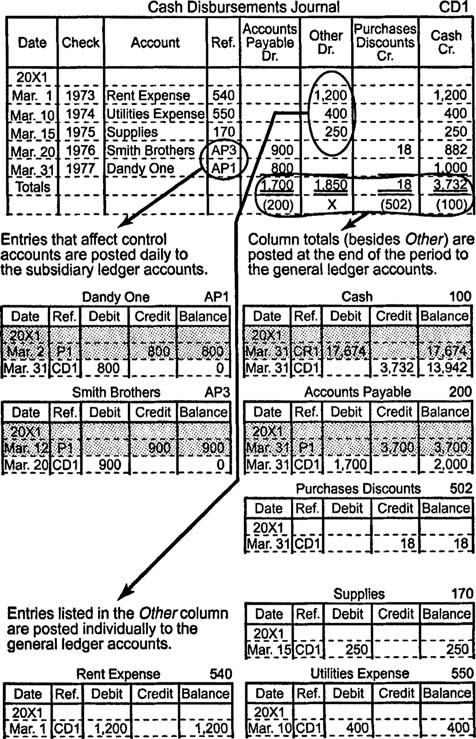

Cash disbursements journal. Transactions that decrease cash are recorded in the cash disbursements journal. The cash disbursements journal to the right has one debit column for accounts payable and another debit column for all other types of cash payment transactions. It has credit columns for purchases discounts and for cash. Since each entry debits a control account (accounts payable) or an account listed in the column named Other, the specific account being debited must be identified on every line.

The nature of each company's transactions determines which columns this journal includes. For example, companies sometimes choose to include separate debit columns for regularly used accounts such as salaries expense, sales commissions expense, or other specific accounts affected by cash disbursements.

Entries that affect accounts payable are posted daily to the individual subsidiary ledger accounts, and creditor account numbers (or check marks if the creditor accounts are not numbered) are placed in the cash disbursements journal's reference column. At the end of the accounting period, each column total is posted to the general ledger account listed at the top of the column, and the account number is placed in parentheses below the total. Entries in the Other column are posted individually to the general ledger accounts affected, and the account numbers are placed in the cash disbursements journal's reference column. A capital Xis placed below the Other column to indicate that the column total cannot be posted to a general ledger account.

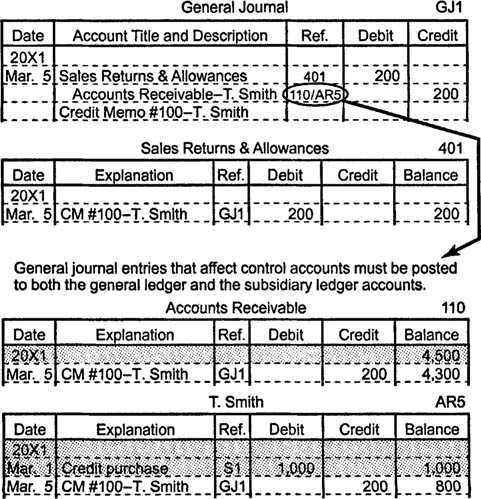

General journal entries. The general journal is used for adjusting entries, closing entries, correcting entries, and all transactions that do not belong in one of the special journals. If a general journal entry involves an account in a subsidiary ledger, the transaction must be posted to both the general ledger control account and the subsidiary ledger account. Both account numbers are placed in the general journal's reference column to indicate that the entry has been posted correctly.