Estimating Bad Debts—Allowance Method

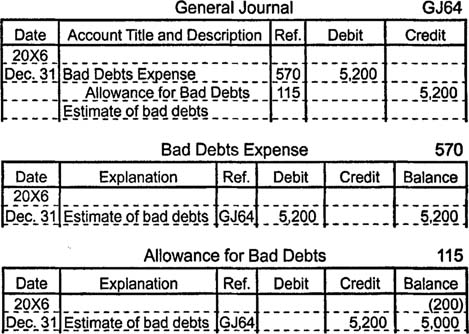

Percentage of total accounts receivable method. One way companies derive an estimate for the value of bad debts under the allowance method is to calculate bad debts as a percentage of the accounts receivable balance. If a company has $100,000 in accounts receivable at the end of an accounting period and company records indicate that, on average, 5% of total accounts receivable become uncollectible, the allowance for bad debts account must be adjusted to have a credit balance of $5,000 (5% of $100,000).

Unless actual write‐offs during the just‐completed accounting period perfectly matched the balance assigned to the allowance for bad debts account at the close of the previous accounting period, the account will have an existing balance. If write‐offs were less than expected, the account will have a credit balance, and if write‐offs were greater than expected, the account will have a debit balance. Assuming that the allowance for bad debts account has a $200 debit balance when the adjusting entry is made, a $5,200 adjusting entry is necessary to give the account a credit balance of $5,000.

If the allowance for bad debts account had a $300 credit balance instead of a $200 debit balance, a $4,700 adjusting entry would be needed to give the account a credit balance of $5,000.

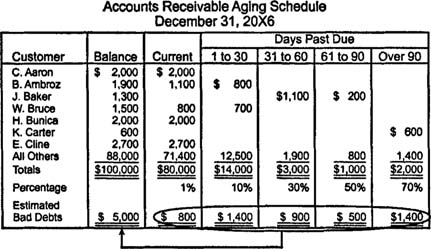

Aging method. In general, the longer an account balance is overdue, the less likely the debt is to be paid. Therefore, many companies maintain an accounts receivable aging schedule, which categorizes each customer's credit purchases by the length of time they have been outstanding. Each category's overall balance is multiplied by an estimated percentage of uncollectibility for that category, and the total of all such calculations serves as the estimate of bad debts. The accounts receivable aging schedule shown below includes five categories for classifying the age of unpaid credit purchases.

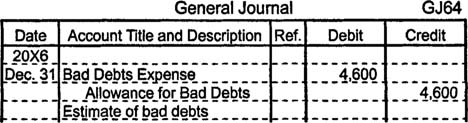

In this example, estimated bad debts are $5,000. If the account has an existing credit balance of $400, the adjusting entry includes a $4,600 debit to bad debts expense and a $4,600 credit to allowance for bad debts.

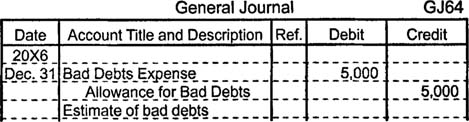

Percentage of credit sales method. Some companies estimate bad debts as a percentage of credit sales. If a company has $500,000 in credit sales during an accounting period and company records indicate that, on average, 1% of credit sales become uncollectible, the adjusting entry at the end of the accounting period debits bad debts expense for $5,000 and credits allowance for bad debts for $5,000.

Companies that use the percentage of credit sales method base the adjusting entry solely on total credit sales and ignore any existing balance in the allowance for bad debts account. If estimates fail to match actual bad debts, the percentage rate used to estimate bad debts is adjusted on future estimates.