Companies sometimes need cash before customers pay their account balances. In such situations, the company may choose to sell accounts receivable to another company that specializes in collections. This process is called factoring, and the company that purchases accounts receivable is often called a factor. The factor usually charges between one and fifteen percent of the account balances. The reason for such a wide range in fees is that the receivables may be factored with or without recourse. Recourse means the company factoring the receivables agrees to reimburse the factor for uncollectible accounts. Low percentage rates are usually offered only when recourse is provided.

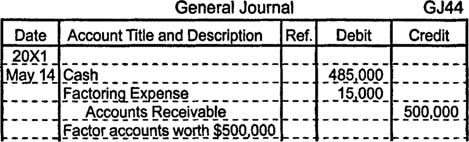

Suppose a company factors $500,000 in accounts receivable at a rate of 3%. The company records this sale of accounts receivable by debiting cash for $485,000, debiting factoring expense (or service charge expense) for $15,000, and crediting accounts receivable for $500,000.

In practice, the credit to accounts receivable would need to identity the specific subsidiary ledger accounts that were factored, although to simplify the example this is not done here.