When a purchaser receives defective, damaged, or otherwise undesirable merchandise, the purchaser prepares a debit memorandum that identifies the items in question and the cost of those items. The purchaser uses the debit memorandum to inform the seller about the return and to prepare a journal entry that decreases (debits) accounts payable and increases (credits) an account named purchases returns and allowances, which is a contra‐expense account. Contra‐expense accounts normally have credit balances. On the income statement, the purchases returns and allowances account is subtracted from purchases.

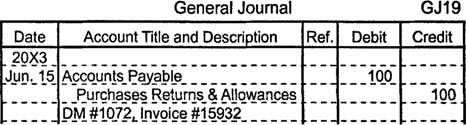

If Music World discovers $100 worth of defective merchandise in the shipment from Music Suppliers, Inc., Music World prepares a debit memorandum, returns the merchandise, and makes a journal entry that decreases (debits) accounts payable for $100 and that increases (credits) purchases returns and allowances for $100.

For reference purposes, the journal entry's description may include the debit memorandum number and the seller's invoice number.