Companies normally use checks to pay their obligations because checks provide a record of each payment. Companies also maintain a petty cash fund to pay for small, miscellaneous expenditures such as stamps, small delivery charges, or emergency supplies. The size of a petty cash fund varies depending on the needs of the business. A petty cash fund should be small enough so that it does not unnecessarily tie up company assets or become a target for theft, but it should be large enough to lessen the inconvenience associated with frequently replenishing the fund. For this reason, companies typically establish a petty cash fund that needs to be replenished every two to four weeks.

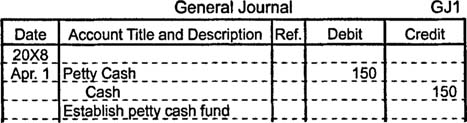

Companies assign responsibility for the petty cash fund to a person called the petty cash custodian or petty cashier. To establish a petty cash fund, someone must write a check to the petty cash custodian, who cashes the check and keeps the money in a locked file or cash box. The journal entry to record the creation of a petty cash fund appears below.

Most companies would record this entry—or any other entry that credits cash—in the cash disbursements special journal, but the illustrations use the general journal to eliminate journal columns that are not relevant to this discussion and to conform with this subject's presentation in most textbooks.

Whenever someone in the company requests petty cash, the petty cash custodian prepares a voucher that identifies the date, amount, recipient, and reason for the cash disbursement. For control purposes, vouchers are sequentially prenumbered and signed by both the person requesting the cash and the custodian. After the cash is spent, receipts or other relevant documents should be returned to the petty cash custodian, who attaches them to the voucher. All vouchers are kept with the petty cash fund until the fund is replenished, so the total amount of the vouchers and the remaining cash in the fund should always equal the amount assigned to the fund.

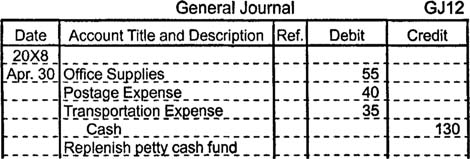

When the fund requires more cash or at the end of an accounting period, the petty cash custodian requests a check for the difference between the cash on hand and the total assigned to the fund. At this time, the person who provides cash to the custodian should examine the vouchers to verify their legitimacy. The transaction that replenishes the petty cash fund is recorded with a compound entry that debits all relevant asset or expense accounts and credits cash. Consider the journal entry below, which is made after the custodian requests $130 to replenish the petty cash fund and submits vouchers that fall into one of three categories.

Notice that the petty cash account is debited or credited only when the fund is established or when the size of the fund is increased or decreased, not when the fund is replenished.

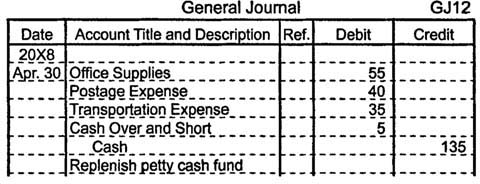

If the voucher amounts do not equal the cash needed to replenish the fund, the difference is recorded in an account named cash over and short. This account is debited when there is a cash shortage and credited when there is a cash overage. Cash over and short appears on the income statement as a miscellaneous expense if the account has a debit balance or as a miscellaneous revenue if the account has a credit balance. In the journal entry below, the vouchers total $130 but the fund needs $135, so the entry includes a $5 debit to the cash over and short account.

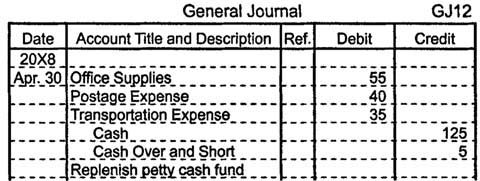

If the vouchers total $130 but the fund needs only $125, the journal entry includes a $5 credit to the cash over and short account.