After journalizing transactions, the next step in the accounting process is to post transactions to the accounts in the general ledger. Although T accounts provide a conceptual framework for understanding accounts, most businesses use a more informative and structured spreadsheet layout. A typical account includes date, explanation, and reference columns to the left of the debit column and a balance column to the right of the credit column. The reference column identifies the journal page containing the transaction. The balance column shows the account's balance after every transaction.

When an account does not have a normal balance, brackets enclose the balance. Assets normally have debit balances, for example, so brackets enclose a checking account's balance only when the account is overdrawn.

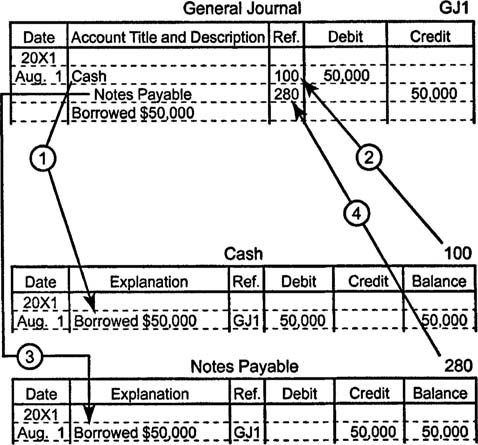

As the numbered arrows below indicate, you should post a transaction's first line item to the correct ledger account, completing each column and calculating the account's new balance. Then you should enter the account's reference number in the journal. Repeat this sequence of steps for every account listed in the journal entry.

Referencing the account's number on the journal after posting the entry ensures that every line item that has a reference number in the journal has already been posted. This practice can be helpful if phone calls or other distractions interrupt the posting process.