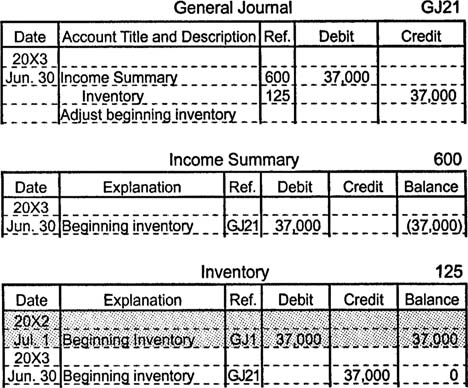

Adjusting the Inventory Account

Under the periodic system of accounting for inventory, the inventory account's balance remains unchanged throughout the accounting period and must be updated after a physical count determines the value of inventory at the end of the accounting period. The inventory account's balance may be updated with adjusting entries or as part of the closing entry process. When adjusting entries are used, two separate entries are made. The first adjusting entry clears the inventory account's beginning balance by debiting income summary and crediting inventory for an amount equal to the beginning inventory balance.

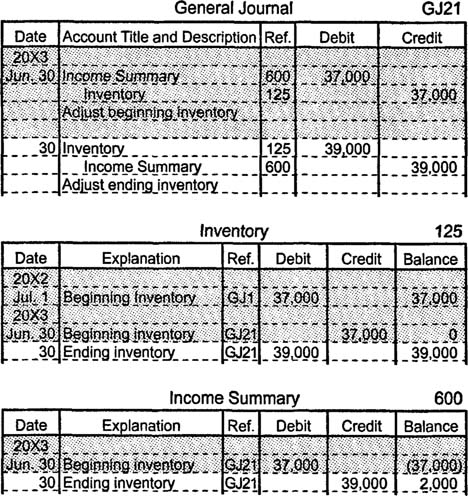

The second adjusting entry debits inventory and credits income summary for the value of inventory at the end of the accounting period.

Combined, these two adjusting entries update the inventory account's balance and, until closing entries are made, leave income summary with a balance that reflects the increase or decrease in inventory.