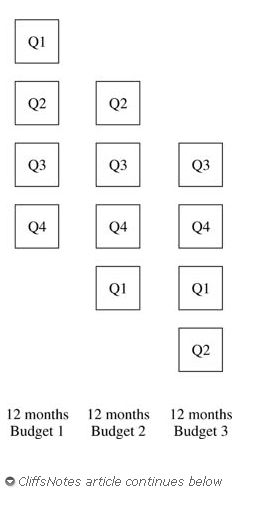

Budgets are part of a company's long‐range planning system. While some portions of a long‐range plan are concerned with the organization in five to ten years, the budget is the short‐range portion of the plan. Most budgets are prepared for a twelve‐month period, sometimes on a rolling basis. A rolling budget is updated quarterly (or as often as management requires the data) by dropping the three months just ended and adding one quarter's data to the end of the remaining nine months already budgeted (see following figure). Rolling budgets require management to keep looking forward and to anticipate changes. ![]()

The master budget consists of all the individual budgets required to prepare budgeted financial statements. Although different textbooks group the budgets differently, the main components of a budget are operating budgets for revenues and expenses, capital expenditures budget, cash budget, and finally the budgeted financial statements, which include the income statement, balance sheet, and cash flow statement.